Bitcoin ETF vs Buying Bitcoin Directly: Which Is Right for You in 2026?

Affiliate Disclosure: This article may contain affiliate links. We may earn a commission at no extra cost to you. All opinions are our own.

Marcus Chen

Senior Crypto Analyst & Educator

Certified Blockchain Professional | Former Wall Street Analyst

Marcus Chen is a cryptocurrency analyst and educator with over 8 years of experience in digital asset trading. He has helped thousands of beginners navigate the crypto markets through practical, actionable education.

Disclaimer: This content is for informational purposes only and should not be considered financial advice. Cryptocurrency investments carry significant risk. Always do your own research (DYOR) before making any investment decisions.

This article contains affiliate links. We may earn a commission at no extra cost to you if you make a purchase through these links. See our affiliate disclosure for details.

Bitcoin ETF vs Buying Bitcoin Directly: Which Is Right for You in 2026?

The Bitcoin ETF vs buying Bitcoin debate has never been more relevant. Since spot Bitcoin ETFs launched in the U.S. in January 2024, billions of dollars have poured into products like BlackRock's IBIT and Fidelity's FBTC — yet plenty of investors still prefer to hold their own keys. Both paths give you exposure to Bitcoin's price. But they work very differently, and the wrong choice for your situation could cost you in fees, taxes, or lost flexibility. Let's break it down.

What's the Actual Difference?

When you buy a Bitcoin ETF, you're purchasing shares in a fund. The fund holds real Bitcoin on your behalf — but you never touch the underlying asset. Think of it like owning a receipt for gold stored in a vault you'll never visit. Your brokerage account shows the position, and you profit (or lose) as Bitcoin's price moves.

Direct Bitcoin ownership is the opposite. You buy BTC on an exchange, then optionally move it to a wallet you control. Your private keys, your coins. No intermediary stands between you and your Bitcoin — which is both the appeal and the responsibility.

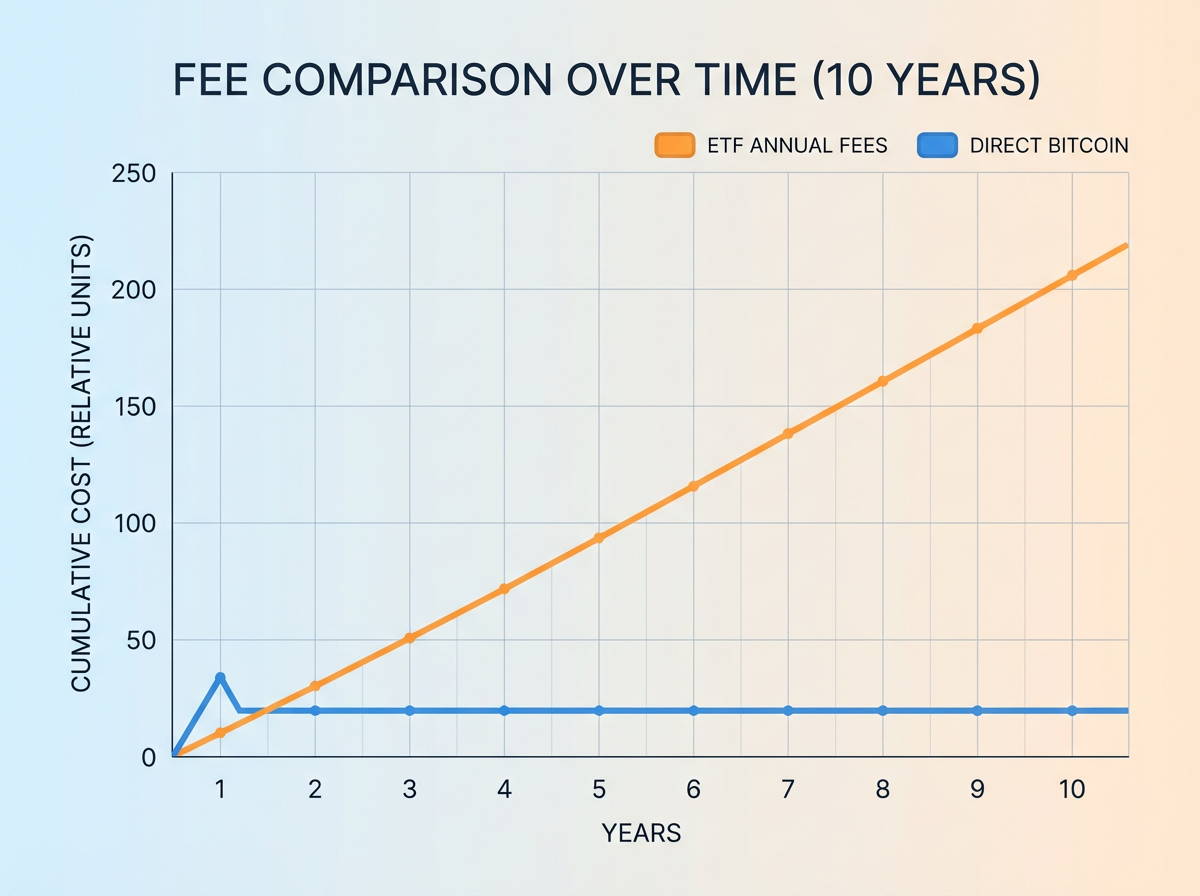

Fee Comparison: Who Pays More Over Time?

This is where the math gets interesting. Bitcoin ETFs charge an annual management fee — typically 0.20% to 0.50% of your holdings. BlackRock's IBIT charges 0.25%. On a $20,000 position, that's $50 per year, every year, forever. Over a decade, you're looking at $500+ in fees before compounding effects.

Direct Bitcoin has upfront costs instead. Exchange fees run 0.5% to 1.5% on most platforms. If you move coins to a hardware wallet, you'll pay a one-time device cost ($79–$249) plus small network fees when transacting. After that initial outlay, holding costs are essentially zero.

The crossover point? Most analyses put it around 7–10 years. Short-term holders often find ETFs cheaper. Long-term HODLers who plan to hold for a decade or more generally come out ahead with direct ownership.

Security: Institutional Custody vs Self-Custody

Here's a stat that should make you think: in 2025, 62% of all crypto theft — roughly $4 billion — came from hot wallets and exchange hacks. That's a real risk for anyone leaving coins on a centralized platform.

Bitcoin ETFs sidestep this problem for retail investors. Custodians like Coinbase Custody hold the underlying BTC in institutional cold storage with multi-signature protocols, insurance coverage, and regulatory oversight. If your brokerage account gets compromised, SIPC coverage (up to $500,000) may protect you — something no crypto exchange offers.

Self-custody flips the equation. A hardware wallet keeps your private keys completely offline, immune to remote hacking. The Ledger Nano X and Trezor Safe 5 are the gold standard here. But you're now the security department. Lose your seed phrase, and your Bitcoin is gone — permanently, with no customer service to call.

Protect your crypto assets with a Ledger hardware wallet — the gold standard in cold storage security.

Tax Treatment: A Major Wildcard

Taxes are where Bitcoin ETFs genuinely shine for certain investors. You can hold ETF shares inside a traditional IRA or Roth IRA. In a Roth IRA, your Bitcoin gains could be completely tax-free at withdrawal. That's a massive advantage if you're investing for retirement and Bitcoin continues its long-term appreciation.

Direct Bitcoin doesn't qualify for most retirement accounts (though some self-directed IRAs allow it with extra complexity). Every time you sell, swap, or spend BTC, it's a taxable event. You'll need to track your cost basis meticulously — or use crypto tax software to do it for you.

One edge direct ownership has: tax-loss harvesting. Unlike stocks, crypto isn't subject to wash-sale rules in the U.S. (as of 2026). You can sell Bitcoin at a loss, immediately rebuy, and lock in the tax deduction. ETF investors can do this too, but the mechanics are slightly different.

Control, Utility, and the "Not Your Keys" Argument

Bitcoin was built on a specific idea: financial sovereignty. The ability to send value anywhere in the world, without asking permission, without a bank or government intermediary. ETF investors get Bitcoin's price exposure — but none of that utility.

With direct Bitcoin, you can:

- Send BTC to anyone globally in minutes

- Use it as collateral for DeFi loans

- Participate in the Lightning Network for near-instant, near-free payments

- Access your funds 24/7, including weekends and holidays

- Hold it outside the traditional banking system entirely

ETF shares trade only during stock market hours. You can't send them to a friend in another country. They're a financial instrument, not a monetary network.

For a deep dive into Bitcoin's monetary philosophy, grab a copy of The Bitcoin Standard — essential reading for every serious crypto investor.

Who Should Choose a Bitcoin ETF?

Bitcoin ETFs make the most sense if you:

- Want Bitcoin exposure in a retirement account — the tax benefits can be substantial

- Are new to crypto and don't want to manage wallets, seed phrases, or private keys

- Invest through a financial advisor who can't hold crypto directly

- Plan to hold for under 5 years — the fee drag hasn't accumulated yet

- Prioritize simplicity over control and utility

Who Should Buy Bitcoin Directly?

Direct ownership is the better path if you:

- Believe in Bitcoin's monetary properties and want actual sovereignty over your assets

- Plan to hold for 10+ years — the fee savings compound significantly

- Want to use Bitcoin for transactions, DeFi, or Lightning payments

- Are comfortable with self-custody and willing to secure a hardware wallet properly

- Want to avoid counterparty risk from ETF providers and custodians

The Hybrid Approach: Best of Both Worlds?

Many experienced investors in 2026 don't choose one or the other — they use both. A common split: 60% in a Bitcoin ETF inside a Roth IRA for tax-free long-term growth, and 40% in direct Bitcoin on a hardware wallet for sovereignty and utility. This captures the tax advantages of ETFs while maintaining real Bitcoin exposure and optionality.

It's not a perfect solution — you're managing two separate systems — but for investors with meaningful Bitcoin positions, the tax savings alone can justify the complexity.

Ready to master crypto trading and make smarter investment decisions? Explore Icoinpro's daily trading signals and education platform — built for investors who want a structured, proven approach.

Key Takeaways

- Bitcoin ETFs are simpler, offer tax advantages in retirement accounts, and provide institutional-grade security — but charge annual fees and give you no actual Bitcoin.

- Direct Bitcoin gives you full control, utility, and lower long-term costs — but requires you to manage your own security.

- The fee crossover point is roughly 7–10 years; long-term holders generally save money with direct ownership.

- A hybrid strategy (ETF in IRA + direct BTC in hardware wallet) is increasingly popular among sophisticated investors.

- Your choice should reflect your time horizon, tax situation, technical comfort, and investment philosophy.

Neither option is universally better. The right answer depends entirely on your goals. But now you have the full picture to make an informed decision.

Knowing what to buy is one thing. Knowing when — that's the skill.

I've watched people hold great coins and still lose money because their entries and exits were off. Structured trading education changed how I approach every position.

The program I recommend to people who ask me is this crypto trading course — it\'s the one I point friends and family to when they\'re serious about learning. Daily lessons, live analysis, and a community that actually helps.

Affiliate link — I may earn a commission at no extra cost to you. I only recommend what I genuinely use.

Disclaimer: The information provided on this website is for educational and informational purposes only. It should not be considered financial or investment advice. Cryptocurrency investments carry significant risk. Always do your own research and consult with a qualified financial advisor before making investment decisions.

Free Crypto Insights

Get weekly trading tips, market analysis, and exclusive strategies delivered to your inbox.