How to Use Aave DeFi Lending and Borrowing in 2026

Affiliate Disclosure: This article may contain affiliate links. We may earn a commission at no extra cost to you. All opinions are our own.

Marcus Chen

Senior Crypto Analyst & Educator

Certified Blockchain Professional | Former Wall Street Analyst

Marcus Chen is a cryptocurrency analyst and educator with over 8 years of experience in digital asset trading. He has helped thousands of beginners navigate the crypto markets through practical, actionable education.

How to Use Aave DeFi Lending and Borrowing in 2026

Aave DeFi lending has quietly become one of the most powerful tools in crypto — letting you earn 3–10% APY on stablecoins or borrow against your holdings without ever selling a single coin. If you've been sitting on ETH or USDC wondering how to put it to work, this guide walks you through exactly how Aave works in 2026, step by step.

As of April 2026, Aave v3 holds over $24.8 billion in Total Value Locked (TVL) across more than 20 blockchain networks. That's not hype — that's real capital from real users who've figured out that DeFi lending beats a savings account by a wide margin. Let's break down how to join them.

What Is Aave and Why It Matters in 2026

Aave is a decentralized, non-custodial lending protocol. You deposit crypto, it goes into a liquidity pool, and borrowers pay interest to use it. You earn a cut of that interest automatically — no bank, no middleman, no waiting for business hours.

The protocol runs on smart contracts, which means the rules are baked into code. Nobody can freeze your funds or change the terms overnight. That's a meaningful difference from what happened with Celsius and BlockFi back in 2022.

Aave vs. Traditional Banks: The Real Difference

Here's a quick comparison that puts things in perspective:

- Bank savings account: 0.5–2% APY, business hours only, KYC required, funds held by the bank

- Centralized crypto lending (CEX): 2–8% APY, counterparty risk, funds held by the platform

- Aave v3: 3–10% APY on stablecoins, 24/7 withdrawals, no KYC, self-custody via smart contracts

The catch? You need a Web3 wallet and a basic understanding of gas fees. That's the learning curve — and it's smaller than most people think.

Getting Started: What You Need Before Using Aave

Before you touch the Aave interface, get these three things sorted:

- A Web3 wallet — MetaMask is the most widely used. OKX Wallet works well too. Download from the official site only, and write down your seed phrase on paper (never digitally).

- Crypto to deposit — USDC, USDT, ETH, or WBTC are the most liquid options on Aave. Start with stablecoins if you want predictable yields without price volatility.

- A small amount of the network's native token for gas — ETH on Ethereum, ETH on Arbitrum/Base, MATIC on Polygon. Gas fees vary wildly by network.

Protect your assets from day one. Serious about security? The Ledger Nano X keeps your private keys offline and safe — especially important when you're interacting with DeFi protocols regularly.

Choosing the Right Network (Ethereum vs. Arbitrum vs. Base)

This decision matters more than most beginners realize. Here's the breakdown:

- Ethereum mainnet: Highest TVL and deepest liquidity. Gas fees run $5–30 per transaction. Best for large positions ($10,000+).

- Arbitrum: Strong TVL, gas fees of $0.01–0.10. The sweet spot for most users — good liquidity without burning money on fees.

- Base: Lowest fees ($0.001–0.05), growing fast. Ideal for smaller positions or if you're just testing the waters.

For most people starting out, Arbitrum hits the right balance. You get solid yields without Ethereum's gas costs eating into your returns.

Step-by-Step: How to Supply Assets and Earn Interest on Aave

Ready to put your crypto to work? Here's the exact process:

- Go to app.aave.com — bookmark this URL. Phishing sites that mimic Aave are a real threat.

- Connect your wallet — click "Connect Wallet" in the top right, select MetaMask (or your wallet of choice), and approve the connection.

- Select your network — use the network dropdown to switch to Arbitrum or whichever chain you've funded.

- Find your asset in the "Supply" section — the dashboard shows available assets with their current APY. USDC on Arbitrum was yielding around 4–7% APY in early 2026.

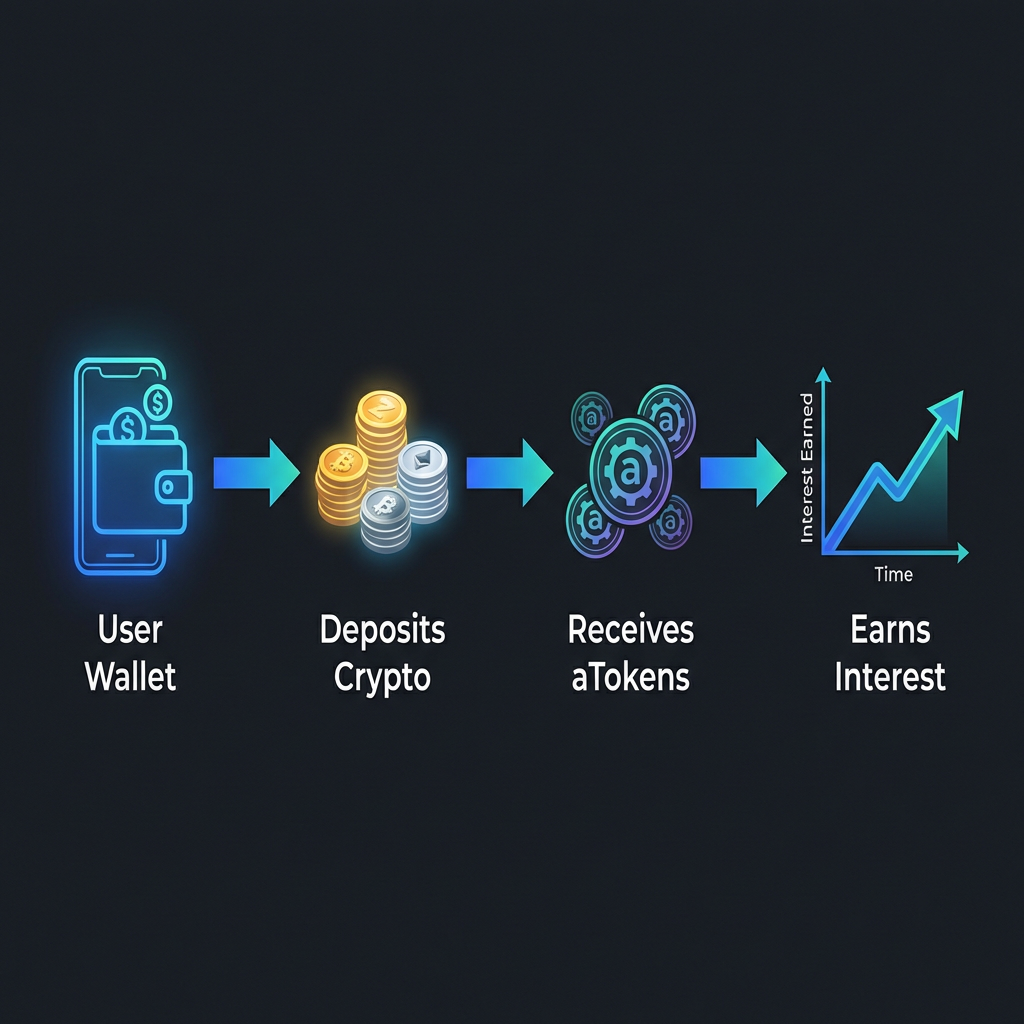

- Click "Supply," enter your amount, and confirm — first-time deposits require an approval transaction (one-time gas fee). Then confirm the supply transaction itself.

- Check your wallet for aTokens — after depositing USDC, you'll receive aUSDC. These tokens represent your deposit and automatically increase in balance as interest accrues. No claiming needed.

Understanding aTokens and How Interest Accrues

aTokens are the receipt for your deposit. If you supply 1,000 USDC, you get 1,000 aUSDC. Over time, that balance grows — say to 1,042 aUSDC after a year at 4.2% APY. When you withdraw, you burn the aTokens and get your USDC plus interest back.

Interest accrues every single Ethereum block — roughly every 12 seconds. You can watch your balance tick up in real time. It's oddly satisfying.

How to Borrow Against Your Crypto on Aave

Borrowing on Aave lets you access liquidity without selling your assets. Classic use case: you hold ETH and expect it to appreciate, but you need cash now. Instead of selling, you deposit ETH as collateral and borrow USDC against it.

Here's how:

- Supply collateral first — your deposited assets automatically become eligible as collateral (you can toggle this in the dashboard).

- Go to the "Borrow" section — select the asset you want to borrow (USDC, USDT, DAI, etc.).

- Enter the amount — the dashboard shows your maximum borrowing capacity based on your collateral.

- Review the borrow APY — this is the interest rate you'll pay. Variable rates fluctuate with market demand.

- Check your Health Factor before confirming — this is the most important number on the screen.

- Confirm the transaction — borrowed funds land in your wallet immediately.

The Health Factor Explained (And How to Avoid Liquidation)

The Health Factor is a single number that tells you how safe your position is. The formula: (Collateral Value × Liquidation Threshold) ÷ Total Debt.

Think of it like this:

- Health Factor > 2.0: You're comfortable. Collateral is worth 2x+ your debt.

- 1.5–2.0: Moderate risk. Keep an eye on it.

- 1.0–1.5: Danger zone. Add collateral or repay some debt immediately.

- Below 1.0: Liquidation. Aave sells your collateral at a 5–10% penalty to cover the debt.

Practical rule: never borrow more than 50% of your collateral value. If ETH drops 30% overnight, a 50% borrow ratio keeps you safe. A 70% ratio gets you liquidated.

Set up price alerts on your phone. DeFi Saver offers automated liquidation protection if you want a safety net.

E-Mode: Borrowing More With Correlated Assets

E-Mode (Efficiency Mode) is a feature for borrowing correlated assets — think USDC collateral to borrow USDT, or wstETH collateral to borrow ETH. Because these assets move together in price, Aave allows up to 97% LTV in E-Mode.

This is useful for stablecoin yield farming: deposit USDC, borrow USDT at 97% LTV, supply the USDT elsewhere for yield. The risk is depeg events — if USDC or USDT loses its peg, your Health Factor collapses fast. Use E-Mode only if you understand the risks.

Aave Fees, Risks, and What to Watch Out For

Aave's fee structure is straightforward:

- Supplying, withdrawing, repaying: Free (only gas fees apply)

- Borrowing: Variable APY, accrues continuously

- Flash loans: 0.05% fee

- Liquidation penalty: 5–10% of collateral

The risks worth knowing:

- Smart contract risk: Aave has been audited extensively and has operated without major exploits on its core contracts since 2020. But no smart contract is 100% risk-free.

- Variable rate risk: Borrow APY can spike during high-demand periods. A rate that was 4% can jump to 15% if utilization hits 90%+.

- Liquidation risk: Crypto is volatile. A sudden market crash can push your Health Factor below 1.0 faster than you can react.

- Stablecoin depeg risk: If USDC or USDT loses its peg, positions using them as collateral or debt can behave unexpectedly.

Start small. Seriously — put in $100 and run through the full cycle before committing larger amounts. The learning is worth more than the yield on a small test position.

Advanced Aave Strategies Worth Knowing

Once you're comfortable with the basics, these strategies open up:

Leveraged ETH staking: Supply wstETH (liquid-staked ETH) → borrow ETH via E-Mode → stake the borrowed ETH → repeat. You amplify your staking yield, but liquidation risk increases with each loop.

Stablecoin yield farming: Supply USDC → borrow USDT via E-Mode → supply USDT to a high-yield protocol. You're essentially earning yield on borrowed money, minus the borrow cost. Works when supply APY > borrow APY.

Leveraged long ETH: Supply ETH → borrow USDC → buy more ETH → supply as collateral. This amplifies your ETH exposure. High risk, high reward — only for experienced users who can monitor positions closely.

Want to accelerate your trading journey? Explore Icoinpro's daily trading signals and education platform — they cover DeFi strategies alongside traditional crypto trading in a structured format.

For a deep dive into Bitcoin's monetary philosophy and the broader crypto ecosystem, grab a copy of The Bitcoin Standard — essential reading for every crypto enthusiast building a serious DeFi strategy.

Key Takeaways

- Aave v3 holds $24.8B+ TVL and offers 3–10% APY on stablecoins with no KYC and instant withdrawals

- Start on Arbitrum or Base to minimize gas fees while learning the protocol

- Supply assets to earn aTokens that automatically accrue interest every ~12 seconds

- Keep your Health Factor above 2.0 when borrowing — never borrow more than 50% of collateral value

- E-Mode enables higher LTV for correlated assets but carries depeg risk

- Always bookmark app.aave.com and use a hardware wallet for significant positions

DeFi moves fast. Your trading skills need to keep up.

Whether you're yield farming or trading tokens, the fundamentals of reading charts, managing risk, and timing entries apply everywhere in crypto. Those skills are worth developing properly.

The program I recommend to people who ask me is this crypto trading course — it\'s the one I point friends and family to when they\'re serious about learning. Daily lessons, live analysis, and a community that actually helps.

Affiliate link — I may earn a commission at no extra cost to you. I only recommend what I genuinely use.

Disclaimer: The information provided on this website is for educational and informational purposes only. It should not be considered financial or investment advice. Cryptocurrency investments carry significant risk. Always do your own research and consult with a qualified financial advisor before making investment decisions.

Free Crypto Insights

Get weekly trading tips, market analysis, and exclusive strategies delivered to your inbox.